Daily Financial News

Don’t Count On JPY Correction; Staying Long GBP/JPY

The path of the potential pace of the JPY decline may still be underestimated by markets, which continue trading the JPY long.

While the 10% USDJPY advance from September lows looks impressive from a momentum point of view, it may no thave been driven by Japan’s institutional investors reducing their hedging ratios or Japan’s household sector reestablishing carry trades.

Instead, investors seemed to have been caught on the wrong foot, concerned about a sudden decline of risk appetite or the incoming US administration being focused on trade issues and not on spending. Spending requires funding and indeed the President-elect Trump’s team appears to be focused on funding. Here are a few examples: Reducing corporate taxation may pave the way for US corporates repatriating some of their USD2.6trn accumulated foreign profits. Cutting bank regulation could increase the risk-absorbing capacity within bank balance sheets. Hence, funding conditions – including for the sovereign – might generally ease. De-regulating the oil sector would help the trade balance, slowing the anticipated increase in the US current account deficit. The US current account deficit presently runs at 2.6% of GDP, which is below worrisome levels. Should the incoming government push for early trade restrictions, reaction (including Asian sovereigns reducing their holdings) could increase US funding costs, which runs against the interest of the Trump team.

Instead of counting on risk aversion to stop the JPY depreciation, we expect nominal yield differentials and the Fed moderately hiking rates to unleash capital outflows from Japan.The yield differential argumenthas become more compelling with the BoJ turning into yield curve managers. Via this policy move, rising inflation rates push JPY real rates and yields lower, which will weaken the JPY. Exhibit 12 shows how much Japan’s labor market conditions have tightened. A minor surge in corporate profitability may now be sufficient, pushing Japan wages up and implicity real yields lower.

JPY dynamics are diametrical to last year . Last year, the JGB’s “exhausted”yield curve left the BoJ without a tool to push real yields low enough to adequately address the weakened nominal GDP outlook. JPY remained artificially high at a time when the US opted for sharply lower real yields. USDJPY had to decline, triggering JPY bullish secondround effects via JPY-based financial institutions increasing their FX hedge ratios and Japan’s retail sector cutting its carry trade exposures. Now the opposite seems to be happening. The managed JGB curve suggests rising inflation expectations are driving Japan’s real yield lower. The Fed reluctantly hiking rates may keep risk appetite supported but increase USD hedging costs.Financial institutions reducinghedge ratios and Japan’s household sector piling back into the carry trade could provide secondround JPY weakening effects

Daily Financial News

What is the best crypto wallet ?

What is the best crypto wallet: a hardware wallet, a software wallet, or a mobile wallet?

In the early stages of learning how to use Bitcoin, the security question arises: how to ensure your coins remain in your possession? Only by generating and storing keys in a way that can be verified can you be certain. It is impossible to be sure no one else has a copy of your keys unless you know they were created properly and stored offline.

Hardware wallets create your keys offline using a random number generator, so they cannot be logged. Additionally, the keys are kept permanently offline, so they cannot be accidentally shared on a network.

In software wallets and mobile wallets, random number generators are often built into the device the wallet is installed on. Since they use inputs like the current time to calculate randomness, they are difficult to verify and generally not secure. Even if your device generates randomness in a secure manner, host the resulting keys on a networked device, and an attacker can extract, view, or intercept them at any time.

It is transparent to verify that open-source hardware wallets create and store randomness securely, and that your keys are kept offline while being protected from threats like phishing. It is different in the case of open-source Bitcoin wallet though.

In addition to protecting against other vulnerabilities, hardware wallets resolve new attacks both progressively and reactively among security researchers. Supporting bug bounty programs ensures that all types of security issues are regularly checked.

What is the best crypto wallet_ a hardware wallet, a software wallet, or a mobile wallet_

Stay more secure everywhere

Hardware wallets have set a new standard for universal cybersecurity, as we discussed above. According to speculators, the future of the internet – dubbed Web3 – will rely on cryptographically secure keys backed up physically. In the cryptosphere, as well as in everyday business, e-commerce, and social media, hardware wallets are essential.

Your assets and identity are both protected offline when you use a hardware wallet for authentication, so there is no counterparty risk.

As a result of forgetting passwords and changing authenticator devices, security has long relied on third parties. Using the open recovery seed standard, users can backup their accounts safely without relying on a third party and recover accounts from any compatible device. Using Shamir backup, the recovery seed is split into multiple equal parts for stronger security.

Keeping in mind that not just crypto can be targeted is important. Similarly, your data can be leaked, resulting in phishing attacks, hostage situations, or compromised devices arriving by mail.

It has become easier and more affordable for everyone to have verifiable security thanks to hardware wallets.

The base layer of crypto security is hardware wallets

By bridging the digital and physical worlds, hardware wallets create digital keys offline and keep them safe. Crypto assets can be controlled with the keys in many ways, such as two-factor authentication, digital signatures, or two-factor authentication.

With open standards, you can ensure the same level of security across any app you use. As a result, dozens of hardware wallet manufacturers have appeared around the world, accelerating the adoption of crypto security and ensuring standards are maintained to ensure your coins remain yours regardless of wallet.

Daily Financial News

Monero Price starts the Selloff, BitcoinCash and Cardano struggle

Table of Contents

Monero Price starts the Selloff, BitcoinCash and Cardano struggle

Monero Price (XMR) tumbled at a double-digit rate today and is likely to continue to fall somewhat , extending its declining trend for a third day straight after hitting a two-month high earlier in the week.

The broader selloff in cryptocurrencies impacted XMR price; the fresh wave of downside volatility in digital currencies was pinged by regulators and the surprise drop in trading volume.

Before the latest crypto market crash, Monero price gained substantial momentum in the last couple of weeks.

it even climbed to the 10th spot in its market capitalization.

n the middle of this month( if launched on time) a spin off or fork of the monero coin called MoneroV will be launched  , people that have monero coins can get 10 moneroV coins for every monero coin. this is always good for the market and Monero went on a small rise. this is now behind us and the prices settled before this announcement was made returning more to its original value.

, people that have monero coins can get 10 moneroV coins for every monero coin. this is always good for the market and Monero went on a small rise. this is now behind us and the prices settled before this announcement was made returning more to its original value.

But for traders and brokers these were a few interesting days where people that saw the market the correct way made good profits

Still Trader’s sentiments overall turned bearish

the main reasons for this are:

crypto exchanges registration with SEC

The U.S. SEC has informed all the domestic cryptocurrency exchanges to get the registration certificate or wait for a crackdown on them.

a crackdown on Japanese exchanges

Japanese authorities are now closely watching digital currencies to protect crypto traders from adverse events, such as Coincheck hack – which resulted in the loss of $500 million worth of coins.

declining trading volume

Lower trading volume is a major factor behind the broader selloff in digital currencies, while the decline of 80% in Google searches indicates the waning popularity of cryptocurrencies.

harsh comments from European regulators.

Regulators started taking actions against cryptocurrencies exchanges to evade illegal activities and price manipulation techniques.

this affects the markets as the hype has settled down.

this affects other currencies in a similar manner as Cardano (ADA), which is the eighth largest cryptocurrency based on market capitalization, plunged more than 6% today to the lowest level since mid-December.

Its market capitalization stands around $5.9 billion, slightly higher from Stellar’s (XLM) capitalization of $5.8 billion.

And Bitcoin Cash (BCH) traded in the range of $1200 in the last of couple week before falling to $1000 level today.

it could be assumed that this will continue to go down till another hype cathes the markets. cryptocurrencies have become already something that is less sexy and more mainstream ,this is good for its development but for those that only invest not so much.

still as a trader you see a volatile market where enough fluctuations happen mostly based on news to make some good trades. good luck

Daily Financial News

Supreme Court Sides With Bits of Gold in Bank Dispute

Supreme Court Sides With Bitcoin Broker “Bits of Gold” in Israeli Bank Dispute

Upon appeal, the Israeli Supreme Court has rejected the closure of Bits of Gold’s banking facilities at Leumi bank, Tel Aviv.

The Israeli cryptocurrency brokerage’s appeal followed a previous ruling against it that has now been set aside by the higher court.

As Israel and many other countries struggle with the accelerated phenomenon of virtual currencies, Leumi Bank recently made the news for being a particularly blunt in its rejection of Bitcoin.

We should of course not be surprised with the banks attitude towards bitcoin or any other cryptocurrency for that matter. keep in mind that the banks become more and more obsolete because of them.

They will keep on loosing money which now they make with ridiculous commissions of work that is fully automated. so they will try to see how they are able to make the operation and acquiring cryptos as hard as possible knowing that they will never be able to stop them.

There is widespread anticipation that the upcoming G20 Summit in March 2018 will produce a global, moderate framework for a regulatory approach. Set against that are persistent hostile stances the world over from banks, asset managers and even governments towards cryptocurrencies.

Now that the countries understand there is money to be made with Taxation in cryptocurrencies they might want to make sure that the banks stay within their lane.

Apart from the Israeli revenue service opting to tax cryptocurrency assets as “properties” and other more positive developments dating back to mid-2017, Israel remains a strange mix of genteel acceptance alongside wildly opposing voices.

There is thus Hope But no decision

Bits of Gold has fought a David and Goliath battle since their banker decided it wanted to steer clear of all cryptocurrency-related business.

On record as recently telling another bitcoin-related trader that they simply don’t want the business, Leumi Bank’s hard-line stance is accumulating bad press. The second-largest bank in Israel appears as discriminatory when analyzing virtual currency traders and other digital coin businesses.

During 2017, a customer made a bank transfer to the Kraken exchange site for buying bitcoin worth $1000. The bank identified the request, halted it, and started investigating.

The elated CEO of Bits of Gold, Youval Rouach said that “The court’s decision enables us to focus on the growth of the Israeli cryptocurrency community.”

The February 26 Supreme Court ruling granted Bits of Gold a temporary injunction against their account closure pending further scrutiny by the bank and other parties. The presiding bench declared that the company had “acted transparently and did not violate any provision of law.”

Calling the bank’s concerns “speculative” and turning an unsympathetic ear to the plaintiff, the ruling does, however, allow for the bank to still close the account on any small technical detail that defies legislation. As a record of a public spat around cryptocurrency’s right to be recognized in many ways, the ruling is seen as a victory for the local cryptocurrency community.

One Small Step Forward

Although not as absolute as nations like China that has opted for draconian bans, Israel is a front line for digital coins’ right not just to exist, but also become assets in the true sense of the word. The Supreme Court noted in its written ruling that Bits of Gold had not made itself guilty of the violation of any standing laws since opening its doors for business.

The Bits of Gold v. Leumi Bank case might become something of a test case once the bank applies its mind in scrutinizing the company’s accounts against the backdrop of existing legislation. The outcome will also be informed by sentiment post the G20 Summit due in March as well as other global regulatory trends.

Now that the countries understand there is money to be made with Taxation in cryptocurrencies they might want to make sure that the banks stay within their lane.

This was First Published by coindesk

Daily Financial News

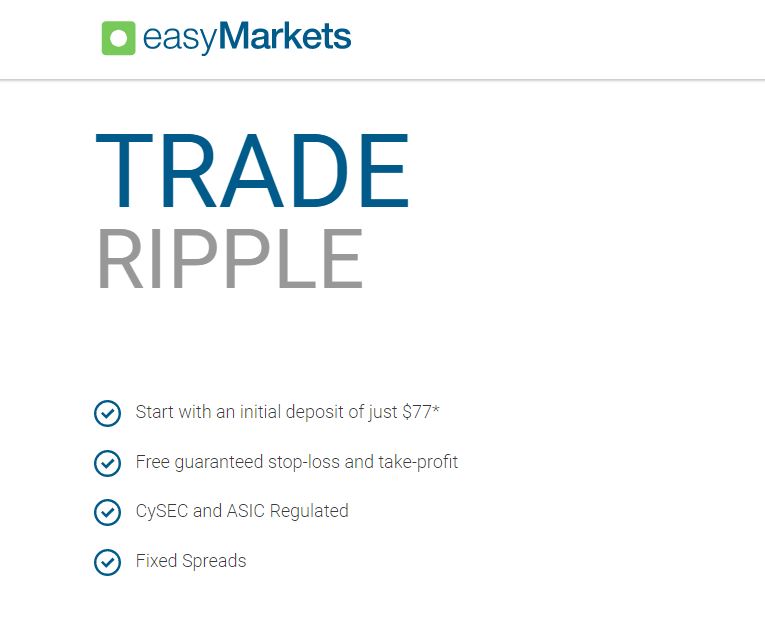

easyMarkets launches Ethereum and Ripple.

easyMarkets launches the crypto-markets’ best kept secret – Ethereum and Ripple.

The crypto markets are the new frontier of trading, we have seen unprecedented movement – from astonishing peaks to abrupt crashes – behaviors and easyMarkets launches Ethereum and Ripple.movements no other instrument experiences or has experienced previously.

Bitcoin was immensely popular when we introduced it to our customers in 2017. After closely following the innovative cryptocurrency markets we found two more immensely interesting (but less visible) cryptos to add to our offerings – Ethereum and Ripple.

easyMarkets launches Ethereum and Ripple.

Ethereum is a blockchain based cryptocurrency like Bitcoin, whereas Ripple is a cryptocurrency payment protocol, touted as a solution to perform payments for institutional clients. Although Bitcoin was undeniably the markets’ star in 2017 – these two crypto-counterparts had equally impressive movements.

Ripple towards the end of 2017 had a notable 33014% overall climb with a market cap of $83.6 Billion. This was assisted by Ripple’s collaboration with institutional users like American Express.

Ethereum had climbed an astounding 8,885% from the beginning of 2017 until the end of that year with a respectable market cap of 69.3 billion. Purely as a cryptocurrency it seemed to even outdo its forefather – Bitcoin – by completing transactions quicker and more effectively.

they have also lowered our spreads on Bitcoin!

Of course, all of their cryptocurrencies include easyMarkets great trading conditions:

Trading Conditions

- There’s zero slippage on the easyMarkets web platform meaning your Ripple trades will be executed at the price you see on your screen.

- You can trade Ripple during its most active times, around the clock, five days a week.

- They got you covered with an in-depth eBook and plenty of other trading education resources.

- Make sure you have an exit plan in place by taking advantage of our 100% guaranteed Stop Loss and Take Profit.

- They cover your deposit and withdrawal fees, so that the amount you deposit or withdraw is the amount you receive.

- Negative Balance Protection means you can never lose more than you invest when you trade Ripple CFDs at easyMarkets.

easyMarkets launches Ethereum and Ripple.

Daily Financial News

Dollar Correction may be Over or Nearly So

The redress in the capital markets started not long after the Federal Reserve climbed rates on December 14. The redress or consolidative stage takes after a generally solid drifting quarter, where moves quickened after the startling triumph by Trump. A week ago despite everything we foreseen the remedy could continue even after the January 4 US employments report indicated more profit development than anticipated. In any case, now after the extra misfortunes, the dollar seems prepared to turn.

Loan costs stay essential to our dollar account. It is not unintentional that the dollar’s drawback move harmonized with a pullback in yields and a narrowing of the US premium. Financing costs might be the place to start our survey of the specialized standpoint.

The 10-year yield tumbled to about 2.30% on January 12, new lows since the finish of November, before recuperating to close at new session highs of 2.36%. Prior to the end of the week, and regardless of on the off chance that anything gentler PPI and disillusioning retail deals figures, the yield climbed another six premise point. The March note fates slowed down at 125-10. It attempted separate sessions sine January 6. Subsequent to falling flat for the third time before the end of the week, an auction guaranteed that brought the agreement toward the week’s low of 124-07, which is additionally a 38.2% retracement of the increases since December 15. The half retracement is found at 123-28, and the 61.8% retracement is at 123-17.

The two-year yield crested on December 15 at 1.30%. It pulled back to close to 16 bp through January 12, when, similar to the 10-year take note of, the yield recuperated and saw finish increases in front of the end of the week. After five closes beneath the 20-day moving normal, the two yield shut above it (~1.21% )before the end of the week. The specialized tone of the March two-year note fates contract is decaying, which is additionally predictable with the consummation of the remedial stage.

The Dollar Index finished a 38.2% retracement of its additions since the US decision on January 12. The little picks up before the end of the week saw the RSI turn higher, while the MACDs and Slow Stochastics are preparing to cross higher also. A move over 102.00 would loan assurance to this view and recommend a retest on the January 11 high almost 103.00. On the drawback, a persuading break regarding 100.65 could goad a move to the following retracement level close to 99.80.

The technicals look assist far from handing over the euro than the Dollar Index. A move above $1.0710 could flag a further recuperation toward $1.0820. The euro has not shut underneath its five-day moving normal, (~1.0590) since January 3. A potential trendline drawn from the current year’s lows comes in close $1.05 on January 16 and completions the week close $1.0575. An infringement of the five-day normal on an end premise or a break of the trendline would likely flag the upside amendment stage for the euro has run its course.

The dollar at first observed complete purchasing in Asia however Japan was on vacation, after the US business information. The greenback was floated from JPY117.00 to JPY117.50. In any case, it was welcomed with crisp offering that eventually drove the dollar to JPY113.75. The specialized markers we utilize have not turned, but rather they are getting extended. A move above JPY115.60 could flag a move in the JPY116.20-JPY116.80 band.

Sterling kept on exchanging intensely. It was the main major to lose ground against the dollar a week ago. Leader May’s affirmation that the UK will lose single market get to sent sterling to $1.2040, its most reduced level since the glimmer crash last October. It figured out how to recoup to $1.2320 yet appeared to draw in merchants. While the five and 20-day moving midpoints cross for the euro and yen, they didn’t have confidence in sterling. May talks again on January 17, however theory before the end of the week that the fall of the administration in Northern Ireland may postpone the activating of Article 50 helped sterling post restorative upticks. All things considered, it flopped again to complete the week above $1.22 which had been the lower end of its range since last October. All things considered, it is conceivable that the $1.2040 low is more solid than the value activity hitherto proposes. The value activity in coming days will clear up the specialized standpoint for conceivably whatever is left of the quarter.

The Canadian dollar expanded its late picks up with a surge around the center of a week ago that conveyed it to the best level and through its 200-day moving normal (CAD1.3100) without precedent for three months. The US dollar achieved CAD1.3030. The greenback immediately recouped into a more steady band amongst CAD1.31 and CAD1.32. The Bank of Canada meets in the week ahead. Late information has been valuable, incorporate work and exchange. The remarks around the stand-pat choice might be more energetic. The Slow Stochastics are ready to turn higher, trailed by the MACDs. The RSI is still overwhelming. A move above CAD1.3200 would settle the US dollar.

The Australian dollar rose 2.5% against the US dollar a week ago. Indeed, it climbed each day a week ago and in eight of the previous nine sessions. It the three-week propel, it has increased around 4.25%. On January 2, it exchanged down to practically $0.7165, and on January 12, it came to almost $0.7520. The high before the Fed’s mid-December rate climb was $0.7525. The $0.7540 region compares to the 61.8% retracement of its misfortunes since the US race. The Australian dollar has not shut underneath its five-day moving normal (~$0.7425) since January 2. Lost this region could be a preparatory sign that the upside rectification is over. The Slow Stochastics look set to cross lower, and the MACDs have all the earmarks of being topping.

The dollar’s ascent through MXN23.00 on January 11 may have finished a move. The MXN21.50 zone drew closer before the end of the week compares to the 38.2% retracement of the current year’s dollar progress (~MXN21.40). The half retracement is close MXN21.30. The specialized pointers are extended. The apparently unusual tweets and a more extensive state of mind of the approaching US Administration deflect numerous from picking a base in the peso.

The February light sweet unrefined petroleum fates contract snapped a four-week progress with a 2.5% drop, in spite of reports proposing Saudi Arabia has cut more yield than it guaranteed. Cost snapped back rapidly from a push underneath $51 a barrel, and the most minimal level since the finish of November. The specialized markers caution of close term drawback chance, yet as it methodologies the base of the range, search for purchasing to reemerge. A move above $53.50 enhances the specialized tone.

The Dow Jones Industrials and the S&P 500 slipped bring down a week ago, while the NASDAQ attached on one percent. Notwithstanding this and the way that the Dow stays underneath the 20k mental level, the hidden tone stays firm. With the S&P 500 under 0.5% from its record, and Dow 20k still in view, there is no sign that value financial specialists are bothered by the absence of detail on assessment change, framework spending, and deregulation. Since the finish of November, the S&P 500 have been exchanging a saw tooth design; substituting weeks are progressing and declining. To augment the example, the S&P 500 needs to close higher one week from now A break of the 2250 territory would debilitate the market’s specialized condition

Daily Financial News

The A to Z of Theresa May’s Brexit as her Vision Speech Nears

For somebody who announced she’ll give no “running analysis” on her Brexit arranges, U.K. Head administrator Theresa May has been very loquacious about Britain’s pending withdrawal from the European Union.

Next Tuesday she is set to state much more as she conveys a discourse on her vision for the separation in the midst of mounting weight from legislators, speculators and administrators, both remote and residential, to substance out her expectations. Her comments will be nearly viewed by cash brokers, after the pound dove because of two of her most huge Brexit analyses.

Six months after she brought office and with under 11 weeks before her own particular due date for activating transactions with the EU, here are her most essential quotes on the key Brexit issues.

Table of Contents

Hard or Soft? Not one or the other

It started July 11, with “Brexit implies Brexit – and will make an accomplishment of it” and it quickly turned into her catchphrase.

May has resolutely declined to take part in the verbal confrontation about whether it will be a “hard Brexit,” which organizes migration controls, or “delicate Brexit,” which shields exchange.

In December, she stated: “Individuals discuss the kind of Brexit that there will be – is it hard or delicate, is it dim or white. Really we need a red, white and blue Brexit: that is the privilege Brexit for the U.K., the correct arrangement for the U.K.”

And after that, on Jan. 9: “I’m enticed to state that the general population who are missing the point are the individuals who print things saying ‘I am discussing a hard Brexit; it’s completely inescapable that it’s a hard Brexit.’ I don’t acknowledge the terms hard and delicate Brexit.”

The Single Market

The head administrator has declined to give a Yes or No reply on whether she needs to haul Britain out of the single market for products and enterprises. The 28 countries in the coalition are individuals from it, as are Norway, Iceland and Liechtenstein.

By the by, she gave her clearest flag yet on Jan. 8 that withdrawal might be the picked pathway when she told Sky News that “we mustn’t consider this as by one means or another ‘we’re leaving participation, yet we need to keep bits of enrollment.’ ”

After a day, after the pound fell in light of those comments, she told columnists in London: “What we are doing will get a goal-oriented, great, most ideal arrangement as far as exchanging with and working inside the single European market.”

While clergymen have said they are concentrate how different nations exchange with the EU, for example, Canada and Turkey, May has said she needs a “bespoke” relationship. “We ought to be driven by what is to the greatest advantage of the U.K. what’s more, what will work for the European Union, not by the models that as of now exist,” she said in July.

Traditions Union

May told Parliament’s Liaison Committee in December that she doesn’t see participation of the traditions union as a “paired choice.” It incorporates Turkey and also the 28 EU individuals and sets no obligations on kindred individuals and a typical duty administration on imports from somewhere else. As a part, however, Britain can’t arrange its own particular exchange bargains.

“There are various diverse perspectives to the traditions union, and there are various distinctive connections that as of now exist in connection to the traditions union, so this is more mind boggling than just saying: ‘Are you in or are you out of the traditions union?”‘ she said.

May’s production of a Department for International Trade and concentrate on fashioning new exchange joins post-Brexit recommends she might need to pull back from the traditions union. Her bureau is part as leaving would mean more organization and obligations for British organizations trading to the alliance.

Movement

May has reliably flagged that the capacity to control movement is a red line in her arrangements. “Give me a chance to be clear: we are not leaving the European Union just to surrender control of movement once more,” she told delegates at the Tory Party gathering in October.

She hasn’t faltered on the issue, telling Sky News this month that she expects to end the flexibility of development of individuals from the EU to Britain, which is one of the center standards of enrollment of the coalition.

“The submission vote was a vote in favor of us to change that opportunity of development, was a vote in favor of us to bring control into our migration framework for individuals originating from the European Union,” she said.

Concerning what framework she may set up, she has discounted an Australian-style focuses framework in which outsiders fit the bill for section contingent upon aptitudes and request. “What the British individuals voted in favor of on June 23 was to bring some control into the development of individuals from the European Union to the U.K.,” May said in September. “A focuses based framework does not give you that control.”

“I need a framework where the legislature can choose who comes into the nation,” she said. “I surmise that is the thing that the British individuals need.”

European Courts

Recapturing power from EU courts is another red line for May.

“We are not leaving just to come back to the purview of the European Court of Justice,” May told the Tory party gathering in October. “We will be a completely autonomous, sovereign nation, a nation that is no longer part of a political union with supranational foundations that can supersede national parliaments and courts.”

She continued effectively expressing the idea.

“Our laws made not in Brussels but rather in Westminster,” she said. “Our judges sitting not in Luxembourg but rather in courts over the land. The specialist of EU law in this nation finished until the end of time.”

She wants to acquaint a bill this year with exchange all EU laws on to the British statute book with the goal of guaranteeing organizations have conviction about what’s to come. Parliament will then be requested that cancelation the laws it couldn’t care less for.

Move and Budget

May has flagged a transitional arrangement might be expected to overcome any issues between the day Britain leaves the EU and the start of an extensive post-separate exchange bargain.

“When we have the arrangement and the new game plans, there will obviously be a need for acclimation to those new courses of action, for usage of some useful changes that may need to happen in connection to that,” she said in December. “That is the thing that business has been remarking on and contending for when, as you say, they utilize the expression about not having a bluff edge. They would prefer not to get up one morning, having had an arrangement concurred the prior night, and all of a sudden find that they need to do everything in an unexpected way.”

On spending commitments, she has declined to preclude proceeding with installments as an end-result of market get to. “What’s vital is that when we leave the European Union, it’s the British government that chooses how citizens’ cash is spent,” May said a month ago.

EU Nationals

May says consenting to ensure the privileges of EU subjects presently living in Britain is a need for her, however is dependent upon proportional assurances for the privileges of Britons dwelling in the other 27 part states. She raised the issue at the European Council in December.

“I made it clear to the next EU pioneers that it remains my target that we give consolation right off the bat in the arrangements to EU nationals living in the U.K. what’s more, U.K. residents living in EU nations that their entitlement to stay where they have made their homes will be ensured by our withdrawal,” she told Parliament. “This is an issue that I might want to concur rapidly, however that unmistakably requires the assention of whatever is left of the EU.”

Parliamentary Involvement

May concurred a month ago to a request from the resistance Labor Party that her arrangements ought to be liable to parliamentary examination before she triggers Brexit. The Supreme Court may yet drive her to hold a parliamentary vote on activating Brexit, with a choice due this month, after May claimed a High Court deciding that she should do as such.

With regards to administrators having an opportunity to talk about the last Brexit bargain, the chief declined three circumstances in declaration to the Liaison Committee to state whether she would give officials a vote.

“It is my goal to guarantee that Parliament has plentiful chance to remark on and talk about the parts of the courses of action that we are setting up,” she told the board.

Resistance and Security

May told the Conservative meeting she needed the detachment understanding “to incorporate collaboration on law authorization and counter-fear based oppression work.”

Scotland and Northern Ireland

May said she’ll talk about with regressed organizations “how the plans will work where we need to take what is a structure right now set out in Brussels into the United Kingdom and perceive the diverse interests of the reverted organizations and the distinctive devolution bargains that are at present set up.”

With respect to Northern Ireland and whether there should be an outskirt amongst it and the Republic of Ireland: ” A ton of work is being done in the matter of how we can guarantee that the game plan for the development of products and individuals over that fringe is not an arrival to the hard outskirts of the past.”

Daily Financial News

On sensitive U.S. stopover, Taiwan leader connects to Twitter

Taiwan President Tsai Ing-wen, cutting a cautious strategic way on her stopovers in the United States, went by the base camp of smaller scale informing administration Twitter Inc (TWTR.N) on Saturday and reactivated an old record.

“Had an awesome visit to @Twitter HQ today. Much thanks to you to @vijaya and group for indicating us around!” read her first tweet from her old record in more than two years. Beforehand she tweeted in Chinese.

There was clashing data before about whether she was opening another English record or restoring the old one.

A source at the meeting said Tsai met with Twitter General Counsel Vijaya Gadde and that CEO and fellow benefactor Jack Dorsey was not present.

Photos of the visit posted online demonstrated the president reactivating her nearness on the informing administration and posturing before the popular photograph that slammed Twitter – 2014 Oscars have Ellen DeGeneres’ “selfie” with top Hollywood VIPs.

Tsai was coming back from seven days in length visit to Central America. In any case, it was her stopovers in the United States that raised more enthusiasm after President-elect Donald Trump said a month ago he would rethink the long-standing “one China” approach, whereby the United States recognizes the Chinese position that there is just a single China and that Taiwan is a piece of China.

He emphasized that probability in a meeting with the Wall Street Journal on Friday, seven days before his introduction. China reacted that the “one China” standard was the non-debatable political reason for China-U.S. relations.

Trump accepted a complimentary call from Tsai after his Nov. 8 triumph, starting shock from China, which trusts the Taiwanese pioneer needs to look for formal autonomy from the territory.

Tsai made a stopover in Houston on Jan. 7 and 8 preceding making a beeline for Central America and arrived Friday night in San Francisco on her way back home. She didn’t seem to have met with any agents of the Trump group amid her short U.S. remains. In any case, in Houston last Sunday, she met with Republican U.S. Representative Ted Cruz and Texas Governor Greg Abbott and started more anger in Beijing.

China had asked the United States not to permit Tsai to enter or have formal government gatherings under the one China arrangement.

Cruz was pointed in his feedback of the Chinese, saying they expected to “comprehend that in America we settle on choices about meeting with guests for ourselves.”

Beijing sees self as overseeing Taiwan a rebel area ineligible for state-to-state relations. The subject is a touchy one for China.

More than a hundred people were assembled outside the Hyatt Regency close San Francisco International Airport, some to challenge and some to bolster the president.

Tsai twisted up her outing with a lunch for 800 individuals from the Taiwanese people group before her booked takeoff for Taiwan toward the evening.

Daily Financial News

Brexit: MPs urge May to clarify trade aims before talks

Theresa May must explain whether she needs the UK to stay in the single market and traditions union, before Brexit talks start, MPs have said.

The Commons Brexit panel said the PM ought to “proclaim her position” by the center of February to permit adequate time for investigation.

In its first report, it said MPs must get a vote on the last arrangement and upheld having a between time bargain if necessary.

Accordingly, the legislature said its objective was a “smooth and methodical exit”.

The leader will give more detail of her goals in a discourse on Tuesday. She has said she will formally trigger the way toward leaving the EU before the finish of March.

Once the Article 50 handle starts, the UK will have two years to arrange the terms of its exit from the EU and framework its future relationship – unless both sides consent to develop the discussions.

The advisory group cautioned that it would be “unacceptable and possibly harming” to both sides if the UK left with no assention and transitional methodology may should be set up in the event that it did.

In its presentation report, the cross-party select board of trustees on leaving the EU – set up in the wake of a year ago’s Brexit vote – made various different suggestions, including:

The privileges of EU nationals in the UK and the other way around must be an “early need” in talks

Parliament and declined congregations must be kept “completely educated” once talks start

Outskirt courses of action between Northern Ireland and the Republic must be settled

The common administration must be “legitimately resourced” to convey Brexit

Co-operation in guard, security and equity ought to proceed

Under weight from Labor, the SNP, Plaid Cymru and some Conservative MPs, the administration consented to set out its essential arranging targets before the procedure starts.

While not anticipating that pastors should trade off their arranging hand, the board said clear positions on the traditions union and the single market were required.

What’s more, any financial evaluations completed on the alternatives identifying with market participation and get to ought to be made open, it said.

The leader has rejected recommendations that the UK confronts a decision between a “hard Brexit” – with more prominent exchange adaptability however the possibility of taxes and traditions obligations – and a “delicate Brexit” where proceeded with market get to would accompany commitments to the proceeded with free development of individuals and to the European Court of Justice.

‘Tremendously intricate’

EU pioneers have said participation of the single market would be incongruent with movement limitations, which Mrs May has demonstrated will be a need. Work MP Hilary Benn, who seats the board of trustees, said it would be “troublesome” to accommodate the two.

“This will be an immensely complex assignment and the result will influence all of us. The administration needs to distribute its Brexit arrange by mid February at the most recent, including its position on participation of the single market and the traditions union, with the goal that it can be examined by Parliament and people in general.”

Transactions on the UK’s separation terms and the premise of its future association with the EU ought to be directed in the meantime, Mr Benn said.

As an “absolute minimum”, he said when of the UK’s takeoff, an “unmistakable system” for the fate of exchange with the EU ought to be in sight.

A between time arrangement might be required, he included, to maintain a strategic distance from the disturbance to business of overnight changes to traditions methods, administrative administrations and migration rules.

“Crazy”

A few Conservative MPs have said a transitional arrangement which keeps on restricting the UK to EU establishments, notwithstanding for a constrained period, would be unsatisfactory.

The advisory group additionally said the administration ought to give an unequivocal duty at an early stage to give MPs a vote on the last arrangement.

Agent John Longworth, a key figure inside the Vote Leave battle, said it was “ludicrous” to assume that transitional plans would be required before talks had even begun.

“Given the leader clarifies now the bearing of travel; that we are leaving the single market and the traditions union, business will have a lot of time to arrange,” he said.

The Department for Exiting the European Union said it would take a stab at the “most ideal” result for the UK.

“We’ve said we will set out our arrangements, subject to not undermining the UK arranging position, before the finish of March and that Parliament will be properly connected with all through the procedure of exit, submitting to all sacred and legitimate commitments that apply,” a representative said.

Broker news

Donald Trump blasts ‘fools’ who oppose good Russian ties

US President-elect Donald Trump has posted a progression of tweets censuring the individuals who contradict great relations with Russia as “‘dumb’ individuals, or nitwits”.

Mr Trump promised to work with Russia “to comprehend a portion of the numerous… squeezing issues and issues of the WORLD!”

His remarks came after an insight report said Russia’s leader had attempted to help a Trump race triumph.

Mr Trump said Democrats were to be faulted for “gross carelessness” in permitting their servers to be hacked.

In a progression of tweets on Saturday, Mr Trump said that having a decent association with Russia was “no terrible thing” and that “lone “idiotic” individuals, or simpletons, would believe that it is awful!”

He included that Russia would regard the US increasingly when he was president

Daily Financial News

Is Euro Periphery Tension Back As A Driver For EUR/USD?

We initially amended our estimates to demonstrate EUR/$ drawback in April 2014, on the method of reasoning that financial outperformance would see the Fed raise rates in front of the ECB, moving rate differentials against the single money. At this crossroads, our 12-, 24-and 36-month gauges for EUR/$ remain at 1.00, 0.95 and 0.90, individually, and rate differentials are still the principle driver for our view.

Intermittently, nonetheless, different variables have risen to drive EUR/$, eminently in mid-2012 when separation hazard was intense and ECB President Draghi made his now celebrated “whatever it takes” discourse, basically pre-reporting the OMT program. This limited Euro outskirts hazard premia (Exhibit 1), driving EUR/$ far above what was legitimized by rate differentials.

With expanded market concentrate on Italy’s banks, we returns to examination we have done in the past on Euro periphery.In specific, we take a gander at family unit and corporate bank stores over the span of the Euro zone emergency.

We presume that stores over the Euro outskirts have held up well, through the many high points and low points of late years, so that late advancements are probably not going to start material surges. The remarkable special case to this photo is Greece, where rising chances of Euro exit in late-2011 and mid-2015 brought about generous store flight. In any case, what is outstanding, once more, is that this store flight did not encourage into virus to whatever is left of the Euro fringe.

A Detailed Lovacrypto Review

Capitalix-It is a good choice in 2024?

Buycryptomarkets Review – top 75 Broker?

Equaledge Review – Demo Account – top 100 Broker ?

Forex Trading Knowledge Questions and Answers

Exallt Review – Demo Account – top 75 Broker ?

Lesson 2 – Pair characteristics (the majors and the crosses), Understanding Forex Pairs

Lesson 3 – Introduction to charting

Lesson 1 – What is Forex and how does It work

What is Price Action Trading and How to Use it

How to Recognize False Breakouts

NSFX Demo Account Review | 2018 Must Read |

- Videos Of interest4 years ago

Lesson 2 – Pair characteristics (the majors and the crosses), Understanding Forex Pairs

- Videos Of interest4 years ago

Lesson 3 – Introduction to charting

- Videos Of interest4 years ago

Lesson 1 – What is Forex and how does It work

- Videos Of interest4 years ago

What is Price Action Trading and How to Use it

- Videos Of interest4 years ago

How to Recognize False Breakouts

- Broker Reviews4 years ago

NSFX Demo Account Review | 2018 Must Read |

- Broker Reviews2 years ago

Stockscale io Review – Demo Account – top 100 Broker ?

- Broker news4 years ago

FX Broker ActivTrades Wins the “Le Fonti Forex Broker of the Year Award”

- Videos Of interest4 years ago

4 Things to Always Do Before You Start Trading

- Broker Reviews2 years ago

Trade.com Demo Account Review | Must Read |